Introducing the Reserve Index Protocol

Positioning Reserve to become the decentralized version of BlackRock, building the infrastructure and brand to support asset-backed currency

Nevin Freeman

Dec 19, 2024

22 min read

ABC Labs is busy building the Reserve Index Protocol, a new piece of software that will unlock the next phase of Reserve’s evolution toward supporting asset-backed currency.

The Ethereum and Base version of the Index Protocol is already undergoing its first of three code audits. The Solana version is currently scheduled to undergo its first audit in January.

The front end interface for this new protocol (including the “zaps” needed to facilitate minting and redeeming) will probably take the longest to finish before public launch. There’s still a lot more code to write for these.

When will it launch?

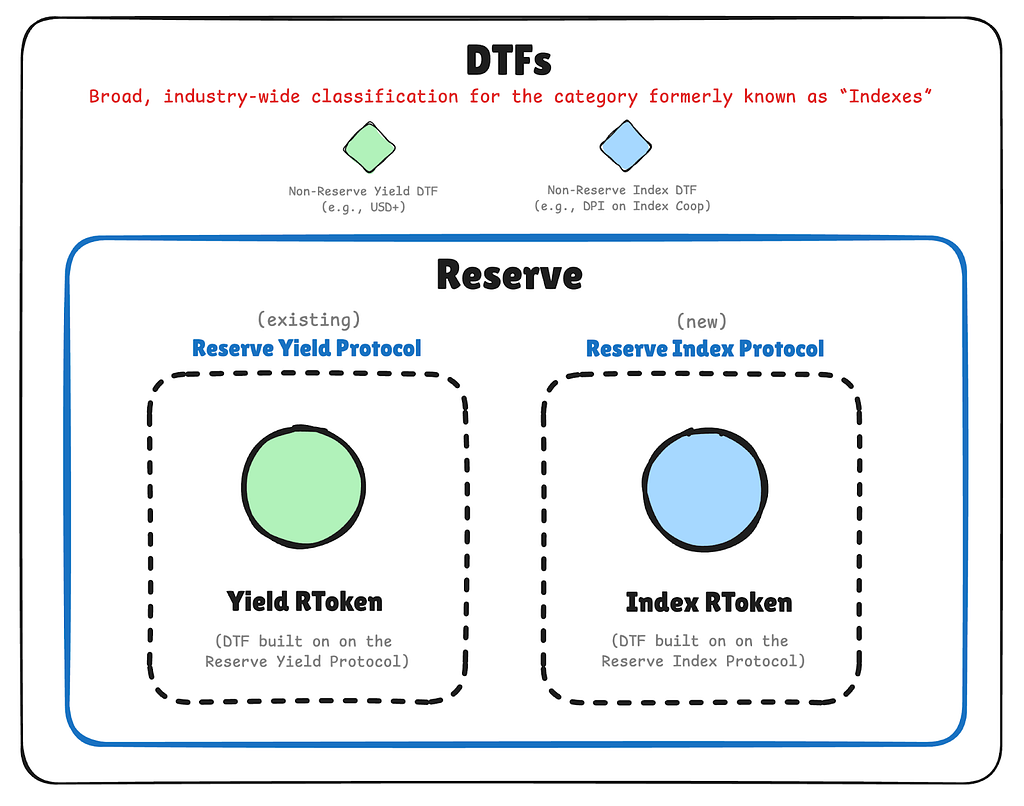

The Reserve Index Protocol will live side-by-side with the Reserve Yield Protocol, which is the new name for the software that powers ETH+, USD3, and all the other RTokens live today.

This release positions Reserve to become the decentralized version of BlackRock — the platform on which thousands of index DTFs can be built by anyone, for anyone.

An “index DTF” is like an index ETF, e.g. the S&P 500 ETF, but in DeFi.

The Reserve Index Protocol lets you bundle together 100+ assets at a time (exact number varies by blockchain), with no need for any oracle price feeds or collateral adapter contracts. This difference is key, as it makes it very easy to create new index DTFs with any token you wish in the basket.

The Index Protocol also adds a powerful new incentive mechanism: creators are given more control over how Index RToken fees are divided up, allowing them to form teams, raise capital, offer liquidity incentives, and so on. I think it’s possible to attract everyone from individual young entrepreneurs up to the largest financial institutions in the world to create and govern DTFs on Reserve technology, and the Index Protocol was designed with this goal in mind.

To ensure that RSR holders are rewarded and incentivized to participate in key ways, Index RTokens collect a platform fee that goes to RSR holders in the form of an RSR burn. (RSR holders ultimately have shared control over this stream of capital; more details below.)

The first half of this post covers the strategy and background for this new phase, and the second half walks through how the new Reserve Index Protocol differs from the current Reserve Yield Protocol.

If you’re more of an auditory person, here’s the community call where I talk through all of the content of this post and answer some questions:

https://www.loom.com/share/2c5fcfa741ff44c7a91fb2b34240f09c

Why asset-backed currency

The Reserve project is based on the premise that access to stable currency should be a human right. Fundamentally, when you do something valuable for society, we believe society should do something of equal value for you in return. That’s not what you get when you save money in an inflationary currency — if your money loses 10% of its value, you’re getting 10% less value back than what you provided to others. And in places like Venezuela where currency has inflated much faster, that effect can be extreme.

In Venezuela we didn’t waste time trying to improve upon the dollar, we offered a USD stablecoin wallet, since it was clear that the dollar was a much better option than the Bolivar at that time. We served about 600k users and 26k merchants who collectively made $5.7 billion in stablecoin transactions on the platform, receiving a special license from the US Department of the Treasury’s Office of Foreign Asset Control covering our operations in Venezuela before having to shut the service down in the face of local regulatory challenges and pressures from Operation Chokepoint 2.0 in the US.

But in the century-long big picture, the US dollar may not always be the answer. The US experienced first-hand the inflationary impacts of monetary policy in recent years, with a peak of 8% annual inflation in 2022, according to BLS.

If the US dollar were to massively devalue (as some think it eventually will), the world could switch to the Euro, Bitcoin, or gold. The Euro has all the same systemic challenges of any large fiat currency, so we might not want it in a world where the dollar has just failed. Bitcoin’s fixed supply means it would have ever-increasing purchasing power in a growing economy, and we’ve seen that it remains highly volatile as it grows in adoption. Gold is perhaps the best option, as its supply can grow in response to growing monetary demand — more gets mined or converted from jewelry when gold value goes up — offering surprisingly stable purchasing power over time.

If you ask open-minded alt monetary economists which of these options is best, they somewhat favor gold, but the final answer you often get is: “let them compete and let the market decide.”

Well the way I see it, when it comes to storing value, the market has already decided. We pretty much all want a diversified portfolio — equities, bonds, real estate, gold, and crypto. You can see this preference in the extreme popularity of index investment products within TradFi.

Reserve’s mission is to fight inflation and expand access to stable currency.

We suspect the solution is asset-backed currency — a diversified portfolio of the world’s assets represented in a single token, so you can store value without inflation over any timespan and transact freely with anyone on the planet.

If we had asset-backed currency alongside bitcoin, gold, and other fiat monies, I believe the market would choose asset-backed currency as its reserve asset if the worst were to happen and the US dollar were to collapse.

Why do I believe this? Well, based on what we already select in order to preserve individual wealth, in some sense the choice has already been made.

How to create asset-backed currency

A central question in creating asset-backed currency is: which assets should back it?

How about we let the market decide. Give everyone access to every combination of assets they might want, and see which combinations bubble to the top.

This experiment has been underway for decades already. In the US, the S&P 500 ETF is the most popular ETF, so we know that people like a broad market index. It performs really well over time, which reinforces its dominance.

But what if we opened up index creation so that anyone in the world could create a new index product, including any financial asset in the world in their index, and then anyone else in the world could put their money into that index if they so chose?

What if each index was a freely transferable token that could be used to settle transactions worldwide in a few seconds?

The market may land on a different choice than the S&P 500 if you give people the ability to use each index in a money-like way and allow indices that span across all borders and asset classes.

And that’s exactly what we are working to do.

The decentralized version of BlackRock

At Monetarium 1 this July I pitched the Reserve ecosystem on a strategy:

- Build Reserve into the decentralized version of BlackRock — make it the largest index platform in crypto, and eventually the largest in all of finance

- Let the process of competitive evolution generate the best diversified stores of value

- Socialize the idea of asset-backed currency more and more as assets on the Reserve platform grow in value over time, so that if the US dollar ever does fall apart, the world is well aware of this option

In the decentralized version of BlackRock, instead of one company creating tons of the biggest index products, an open platform allows thousands of people and companies to create them. In fact, ABC Labs, which writes software to make this possible, has never created an index product itself, and does not intend to.

Note that even if Reserve tokens only become popular index products and are never used as money, ecosystem participants still stand to benefit, so this strategy does not incentivize RSR holders to fight against the US dollar. That’s important to me because the idea here is to build a backstop in case the world needs it, not to do anything that would weaken the current system.

This strategy received full support from everyone who has commented on it, so we all seem to be going full-force ahead. Let’s do it!

DTFs

“DTFs” are like ETFs but in DeFi.

Decentralized token folios.

Like an ETF, each unit is redeemable 1:1 for the basket of underlying assets. The difference is that instead of going to an investment company for redemption, you go to a smart contract, and instead of only market makers being allowed to redeem, anyone can. Since all of the underlying tokens in a DTF are held in a smart contract, no company is in custody, only code. (Some tokenized RWAs still are held by a company that issues the token.)

Another big difference between ETFs and DTFs is that DTFs can have decentralized governance, or no governance at all.

With an ETF, the issuer is the investment company that manages the assets.

With a DTF, you can be the issuer, since anyone can mint or redeem just by interacting with the smart contract, and you can be a governor, since in most decentralized governance approaches anyone can buy governance tokens and participate in guiding the asset selection.

Existing RTokens are DTFs. There are many other projects offering or working on offering DTFs as well. The biggest so far has been the DeFi Pulse Index, which reached a market cap of $236M during the last market cycle, according to CoinGecko.

At this point in time, Reserve is the largest DTF platform by TVL.

ETFs are huge in TradFi. As DeFi grows, I expect that DTFs will be huge as well. This is of course speculation as it hasn’t happened yet, but I don’t see why the same reasons for ETF popularity will not apply.

The initial wedge

For DTF investing to get big, I suspect there will need to be one type of DTF that really takes off and leads the way. So which type might that be?

It may be similar to TradFi — a broad market index, like Coinbase’s COIN50 or CoinDesk’s CD20, implemented onchain for people to buy and hold.

It may be a thematic index, which have also taken off in TradFi.

Maybe it’s baskets of memecoins.

Maybe it’s sector indices — AI, DeFi, DePIN, DeSci, GameFi, etc.

Maybe it’s more complex DeFi positions that generate yield along with their diversification.

An additional Reserve protocol

In order to serve this use case, we’re launching a new protocol.

Going forward, there will no longer be just one Reserve protocol, there will be two:

- The Reserve Yield Protocol (which exists today)

- The Reserve Index Protocol (launching soon)

These two protocols both allow for the permissionless creation of DTFs, but they have different strengths and weaknesses, since they are built for different purposes.

We’re purpose-building the Reserve Index Protocol for what we think is the next phase of DTFs in crypto: volatile index baskets that can include everything from Bitcoin to memecoins you deployed an hour ago.

The Reserve Index Protocol does not replace the Reserve Yield protocol.

Think of them like two models of car produced by one car brand. A pickup truck is good for hauling and a sports car is good for tight turns; the car brand offers them year after year to different market segments

The two protocol models will co-exist to support index DTFs and yield DTFs. For example, USD3 and ETH+ are both yield DTFs that will continue to run on the Reserve Yield Protocol.

The Index Protocol will be deployed on Base and Ethereum first, with a Solana implementation soon after. It may be deployed elsewhere in the future.

The differences between the two protocols are explained below!

An update on terminology

We have a lot of new terminology in play to make all of this clear and easy to talk about. We’re changing the language within Reserve as well as overall in the industry.

Main definitions:

- DTF — Decentralized Token Folio — any token that is redeemable 1:1 for a basket of other tokens, regardless of which protocol or project created it. Not specific to Reserve. “Like an ETF but in DeFi.”

- Yield DTF — a DTF that is designed to capture yield, e.g. ETH+ or USD3. Not specific to Reserve; e.g. “USD+” from Overnight Finance is also a yield DTF.

- Index DTF — a DTF that is designed for broad, diversified token exposure. The DeFi Pulse Index (DPI) from Index Coop + Set Protocol was the most successful index DTF last cycle, for example.

- Reserve — when referring generically to the technology behind Reserve, you can just say “Reserve.” For example, “that DTF runs on Reserve.” It no longer makes sense to say the Reserve protocol, as there is not only one.

Technical term definitions:

- Reserve Yield Protocol— the existing protocol that ETH+, USD3, and other existing RTokens run on.

- Reserve Index Protocol— the new protocol model we are introducing in this blog post and launching soon.

- Yield RToken — a yield DTF built on the Reserve Yield Protocol. This is a bit of a technical term that may not get used all that much; within the main Reserve interface I expect they’ll just be called “yield DTFs.”

- Index RToken — an index DTF built on Reserve. This is a bit of a technical term that may not get used all that much; within the main Reserve interface I expect they’ll just be called “index DTFs.”

How the Reserve Index Protocol differs from the Reserve Yield Protocol

Note: this description is for Reserve project members who are already familiar with the current Reserve protocol. When the Index Protocol is released, it will be accompanied by documentation for folks who know nothing about Reserve.

In a nutshell, the Reserve Index Protocol:

- lets you bundle together any tokens, with no need for collateral plugins specifically written for each token in the basket

- allows for very large baskets of tokens (50+ on Ethereum, and about 100+ on Base)

- distributes one portion of the fee income to governance token holders and the other portion of the fee income to RSR holders, via burning RSR or RSR LP tokens (and in the future, may distribute a portion to an RSR-governed DAO treasury, should RSR holders choose)

- charges fees to RToken holders as a percentage of TVL of the RToken instead of a percentage of yield generated on the collateral

- lets you use any token for decentralized governance, including but not limited to RSR; you can govern with RSR, create a brand new governance token, or bring an existing token and give it governance rights — read below for the motivations behind this incentive design

- does not include RSR overcollateralization

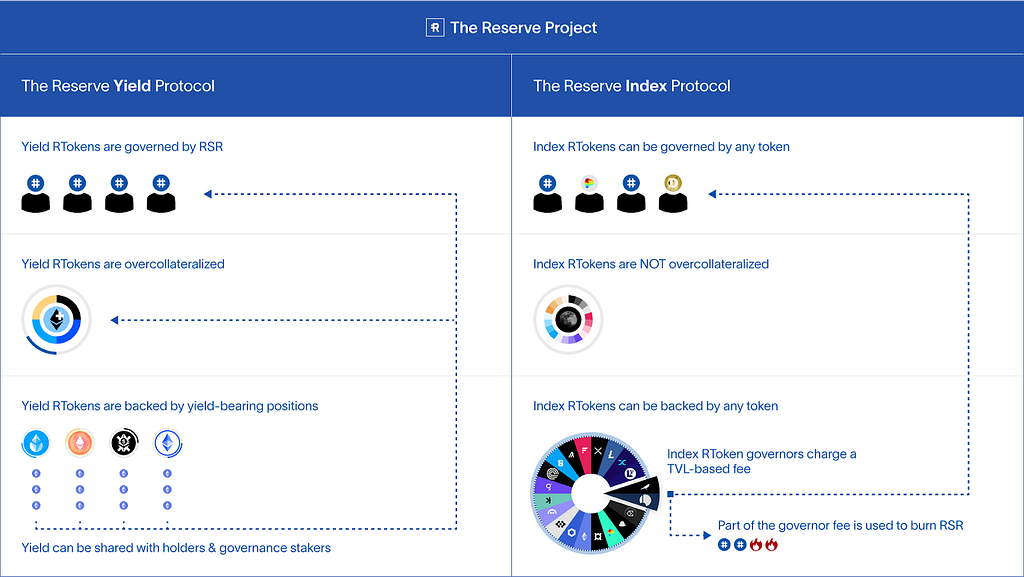

You can start to get an idea of the differences in this simple diagram:

Let’s walk through these design choices one by one in detail.

1. Adding a platform fee which goes to burning RSR

Of the fees charged to holders of Index RTokens, a portion is taken off the top by the protocol itself and goes to burning RSR.

Yes, we are bringing back the RSR burn 🔥🔥🔥

A platform fee schedule will be released at launch.

RSR holders will ultimately have control of where the platform fee revenue goes. The main options are:

- Direct burn: 100% of fees go to RSR burn

- LP burn: fees are converted to DEX liquidity tokens for RSR, which are burned — the reasons to potentially prefer burning LP tokens instead of RSR directly are nuanced and this warrants community discussion to decide what we prefer

- RSR treasury: fees are stored in a treasury controlled by RSR holders

As you digest the design choices below, you’ll see why we reached this conclusion. A platform fee guarantees that RSR holders would benefit from Index RToken growth and usage, should that occur. I’ll cover the governance roles RSR holders are expected to play below.

2. Allowing Index RToken creators to use any token to govern an Index RToken

Yield RTokens have so far all been governed by staked RSR.

(Technically speaking, a Yield RToken’s governor can be any smart contract you specify, so someone could create one that was governed by some other token, but so far nobody has been enterprising enough to do that. It would require technical sophistication.)

Index RTokens, by contrast, will make it easy for their creators to select any token they want, including a brand new token they’ve just created, as the governance token.

An Index RToken’s governance token will be able to charge a governance fee to RToken holders, so the bigger the RToken gets, the more revenue the governance token will generate.

The reason to allow this, in short, is to create an extremely powerful incentive to attract all the best DTF creators and distributors in the next decade to build on Reserve.

Imagine for a minute that Ethereum required that every app built on top of it could only use Ether as its governance token, and that all value from each app would thus have to accrue to ETH.

On one hand, if all apps on Ethereum suddenly paid out all their value to ETH, that would make ETH even more valuable than it is today.

On the other hand, if it had worked this way from the start, way fewer teams would have ever built apps. Only existing large ETH holders would have had the incentive to do so. It would have been extremely difficult to raise new capital and incentivize new teams to build new projects.

I think if Ethereum had worked that way it would have quickly been eclipsed by competitors that allowed builders to make their own tokens.

I believe this same logic will apply to the universe of DTFs.

Imagine this: you have a great idea for a new DTF. You can create it pretty much for free, and when you do, you mint a brand new governance token along with it. That governance token is yours to hand out to team members, partners, or investors in order to supercharge the launch of your DTF. You can stream it to DTF users as an incentive to get early users, or offer it to AMM liquidity providers to bootstrap liquidity for your DTF. And over time, your DTF develops a committed group of governance token holders who have an affinity for that particular DTF. They want more people to use that DTF, because the bigger it gets, the more valuable their governance token is. So what do they do? They do what every crypto community does: they shill! They talk not only about their own governance token and why it’s great, but about the DTF it’s connected to, and why that’s great. Now you have crypto’s decentralized marketing machine working for your DTF. And it may not even really be your DTF by this point. Maybe you created it on a lazy summer afternoon and put some energy in for a few months, then decided to sell your portion of the gov token and move on. It doesn’t need you — it has a whole thriving base of gov token holders who are incentivized to make it great and grow it.

Or imagine this: TradFiGiant, Inc. decides they want to get into the DTF game. They assign a team to study all the existing tech and conduct a “build or buy” analysis, to determine whether to make their own competing protocol or build on top of existing tech stacks. The team looks at Reserve first since it’s the biggest DTF protocol (true today, and hopefully indefinitely!). They see that they can create DTFs on Reserve and retain a good share of the fees for themselves via holding their own governance token. They work out a plan to launch TradFiGiant Token (TFGT) and use it as the gov token for all the DTFs they deploy on Reserve. They are happy to build on the industry leading tech stack instead of creating something from scratch, and the Reserve ecosystem is happy to host them and collect the platform fee as their DTFs grow. The more TradFiGiant markets their DTFs to their existing customer base, the more platform fees RSR holders get to direct, as described in section 1.

So you can see: in this vision, RSR remains the central asset in the Reserve ecosystem, just like ETH is the central asset in the Ethereum ecosystem. And by letting Index DTF creators bring their own tokens to the table, we invite WAY MORE people and companies to build on Reserve, just as Ethereum did from the start.

There are TONS of possibilities here.

- Existing memecoin communities can use their memecoin to govern DTFs.

- Existing DeFi projects can use their governance token to govern DTFs.

- Accelerators can form to incubate DTFs in exchange for 7% of their governance token.

- Every DTF with a brand new gov token can choose whether to have a bonding curve, a dutch auction, an airdrop, farming rewards, a private round, vesting schedules, etc.

Just as the giant mess of projects deployed on Ethereum have brought us some great tokens and some crappy ones, not every DTF gov token on Reserve will be something you’ll want to hold. But, in my vision of it, some really will be.

The obvious tradeoff is that any fees that go to some other governance token are not going to RSR holders. But I’m betting that gives us RSR holders a smaller slice of a much larger pie.

The near-term goal is, after all, to become the decentralized version of BlackRock. To be far and away the number 1 DTF platform. To be the Ethereum of DTFs.

Note that it is uncertain whether this will come to pass. We can design the software to create incentives, but many broad market forces have a lot of influence over the eventual outcome. As an ecosystem participant, you are the one with the power to create and participate in great DTFs and impact how this all turns out!

3. RSR’s role in governing within the Reserve ecosystem

RSR has three governance roles to play in the Reserve ecosystem:

- Continuing to overcollateralize and govern Yield RTokens

- Governing Index RTokens deployed by RSR holders

- Meta-level governance within the Reserve ecosystem

Let’s break these down one at a time.

-

RSR will still be used to overcollateralize and govern Yield RTokens. This is pretty straightforward — nothing’s changing with the Yield Protocol, so as long as Yield RTokens in their current form keep seeing demand, RSR holders will continue to stake on them, govern, and earn staking rewards.

-

Like any other token, RSR can be used to govern any Index RToken. For existing RSR holders, deploying new DTFs with RSR as the governance token is a way to bring even more value to RSR. Such DTFs will benefit from an engaged and savvy community of governors, and may naturally receive the most support from people and companies that hold a lot of RSR. So we may see many Index RTokens deployed with RSR as the governance token. It’s worth noting that even Index RTokens that are not governed by RSR still generate platform fees that go to burning RSR or other uses as elected by RSR holders.

-

Although this plan is still in the discussion stage (publicly and within ABC Labs), there is an intention in the ecosystem to create a meta-level RSR DAO. Key likely responsibilities of this meta-level DAO include: directing protocol fees to burning RSR or other uses, governing which smart contracts existing RToken governors are allowed to update to (for greater system-wide security), governing the use of RSR emissions, and governing platform fees that are charged to Index RTokens.

I started by covering the design choices that most directly interface with RSR holders since RSR holders will read this article most closely. But let’s now turn to some of the choices that will be most relevant to making Index DTFs on Reserve a great product for users!

4. Allowing any token with no collateral adapter needed

For Yield RTokens, the protocol needs to know the price of each collateral asset at any point in time, because it needs to be able to tell when collateral has appreciated or defaulted.

Say you have an RToken with cUSDT (USDT lent out on Compound) as backing. The protocol has to be able to tell that the cUSDT gained in value via the yield that’s accruing to that position in order to calculate how to distribute the value of that underlying yield.

Similarly, if USDT were to de-peg, the protocol has to know this somehow in order to respond by trading out into other collateral and auctioning the right amount of staked RSR to make up the difference.

Requiring pricing info means that each collateral asset must have an oracle price feed. But oracles cost money to maintain and only exist for a small minority of tokens out there, given how quickly new tokens are being created these days.

Requiring a price oracle, in a world with different oracle providers, means that each collateral asset requires a collateral plugin smart contract that defines its oracle price feed so the protocol can understand it. This means a nontechnical person can’t add a new collateral asset to an RToken until a dev has taken the time to write this (simple, but still technical) new contract.

This means that the Reserve Yield Protocol has a more limited universe of potential collateral tokens. That’s fine for its main purpose, but when building index DTFs in DeFi it’s much better if creators and governors can easily add any token out there to the basket.

Thus, in order to allow any token to be easily usable as collateral, the Reserve Index Protocol was designed to operate without needing to know any prices of any collateral assets.

This choice is the central defining premise of the Index Protocol, around which all other design choices were made.

The Index Protocol initially will be deployed on Ethereum, Base, and Solana. You’ll be able to bundle tokens within each blockchain. That can include tokens that are bridged from other blockchains, but Reserve will not have any additional bridging capability to offer.

Now let’s explore some of the resulting features that follow from this premise:

5. Removing RSR staking and overcollateralization

Without pricing info on collateral assets, it’s not possible for the protocol to detect defaults, since those are defined in terms of price deviations.

However, for the near-term index DTF use case, we’re betting that overcollateralization is less important, for two reasons:

Reason 1: many of the collateral assets included in an index DTF in today’s market will be native tokens, which have no risk of default. Take for example a memecoin you just created — it’s just a token, not pegged to anything else, so one token is always one token, period. Its price does not relate to or depend on any other asset, so there is no way for it to “de-peg.”

Reason 2: prospective index DTF users say in product interviews that they are fine taking the risk of bridged or wrapped assets.

The main tokens in index DTFs that could de-peg are bridged or wrapped assets, e.g. WBTC or bridged Bonk on Base. People told us they didn’t mind the “bridge risk” for the convenience of being able to hold a DTF that bundled many assets across chains.

And this makes sense. In the case of a yield DTF like USD3 or ETH+, the whole point is to hold a token that is “up only” with respect to its reference asset (in this case USD or ETH). Any case of loss relative to that asset would be really painful. And as we saw with the USDC de-peg early on in the life of eUSD, the default response mechanism worked really well!

For index DTFs, users are more interested in overall gains, irrespective of any specific reference asset. So the low risk that a wrapped collateral asset may de-peg at some point in the case of a bridge hack seems like a low-priority issue.

This choice means that there is no need for RSR to be staked on Index RTokens.

(In principle, an Index RToken could implement overcollateralization for the more established collateral assets that have oracle price feeds and are bridged or wrapped, such as WBTC. So if there is demand for this feature, a future version could bring the best of both worlds. However, it would have added a lot of code complexity and taken a lot longer to build, so didn’t seem like the right tradeoff to include at this point.)

6. Charging governance fees as a percentage of TVL

Like most index ETFs, it makes sense for index DTFs to charge a fee to users as a percentage of holdings.

If you hold $100 in an Index RToken and it charges holders an annual 1% fee, you will pay $1 per year in fees.

If it appreciated 20% in that year, your $100 would have turned into $120, and $1.20 would be deducted, leaving you with $118.80. (Technically it would happen continuously and the math would be ever so slightly different, but you get the idea.)

In contrast, Yield RTokens charge fees as a percentage of yield generated. This makes sense, given that their main value prop is yield.

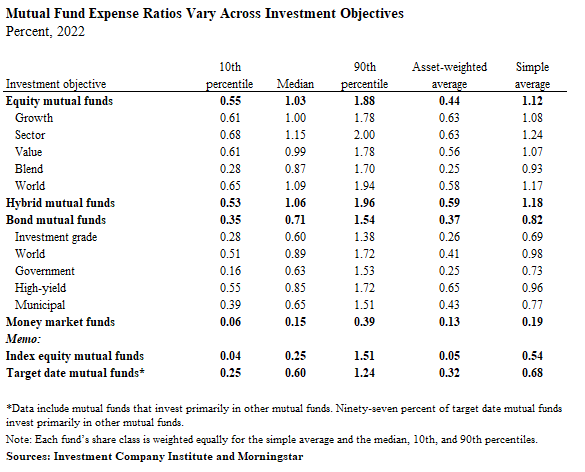

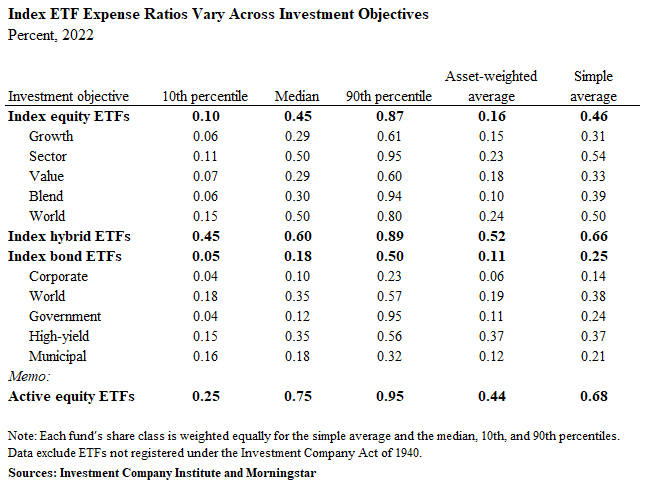

For reference, TradFi fees, also called “expense ratios”, vary a lot according to research conducted by the Investment Company Institute (ICI):

Governance fees can vary depending on the DTF. A large-cap crypto index that rarely changes or rebalances may charge a very low fee. In contrast, a memecoin index with frequent basket changes hunting for the newest meta may charge 5% or even more, and that may be totally worth it. For the DTF holders searching for 10–100x opportunities, a high-fee, high-variance DTF may achieve that outcome.

Part of the fee charged to RToken holders goes to the platform (i.e. RSR holders) and part goes to the RToken’s governors. These are called the platform fee and the governance fee. Governors cannot remove the platform fee.

Because a fee that’s a flat percentage of all of the tokens in the basket can be calculated in terms of number of tokens regardless of their market price, no collateral pricing info (and hence no oracle price feeds) are required for these fees.

7. Allowing for very large collateral baskets

The Yield Protocol contains quite a lot of code to do the fancy accounting necessary to track yield, monitor tokens for default, make use of staked RSR in defaults, and so on. The Index Protocol is comparatively simple.

- The Yield Protocol is 10,052 lines of code.

- The Index Protocol is only 1,053 lines of code!

(both numbers for the Ethereum versions)

The reduction in lines of code means lower gas usage and fees on minting and redeeming. This means you can have much more diverse collateral baskets.

On Ethereum L1:

- Yield RTokens can handle about 10 collateral tokens before they become too computationally expensive

- Index RTokens will be able to handle 50+ collateral tokens before they become too computationally expensive

On Base:

- Yield RTokens can handle about 20 collateral tokens before they become too computationally expensive

- Index RTokens will be able to handle 100+ collateral tokens before they become too computationally expensive

On Solana:

- As development is still underway, this number is not known yet.

8. Deploying the Index Protocol on Solana

We believe the crypto space is ready for Index DTFs, and clearly there is a lot of action on Solana, so it made sense to deploy the Reserve Index Protocol there.

For now there is not a near-term plan to deploy the Yield Protocol on Solana. It’s complex enough that this would be quite a lot of additional development work.

Timelines

As I said in the introduction:

The Ethereum and Base version of the Index Protocol is already undergoing its first of three code audits. The Solana version is currently scheduled to undergo its first audit in January.

The front end interface for this new protocol (including the “zaps” needed to facilitate minting and redeeming) will probably take the longest to finish before public launch. There’s still a lot more code to write for these.

When will it launch?

SHARE THIS