Reducing RSR emissions: hardcoding the supply curve to emulate Bitcoin

Fostering growth, giving RSR holders clarity and predictability for the long term, and positioning RSR to be a sound store of value

Nevin Freeman

Aug 14, 2024

21 min read

Thank you to everyone who has contributed a perspective on long-term RSR emissions!

We’ve had about 35 different perspectives and ideas proposed on the forum, and the Confusion Capital team has thought through each one and shared feedback (in these two comments). We also gave a presentation at Monetarium on the topic, which you can check out if you’d like to understand the reasoning in this blog post more fully:

The update

Today, Confusion Capital is announcing that RSR emissions will be set on a deterministic schedule which emulates the emissions curve of Bitcoin.

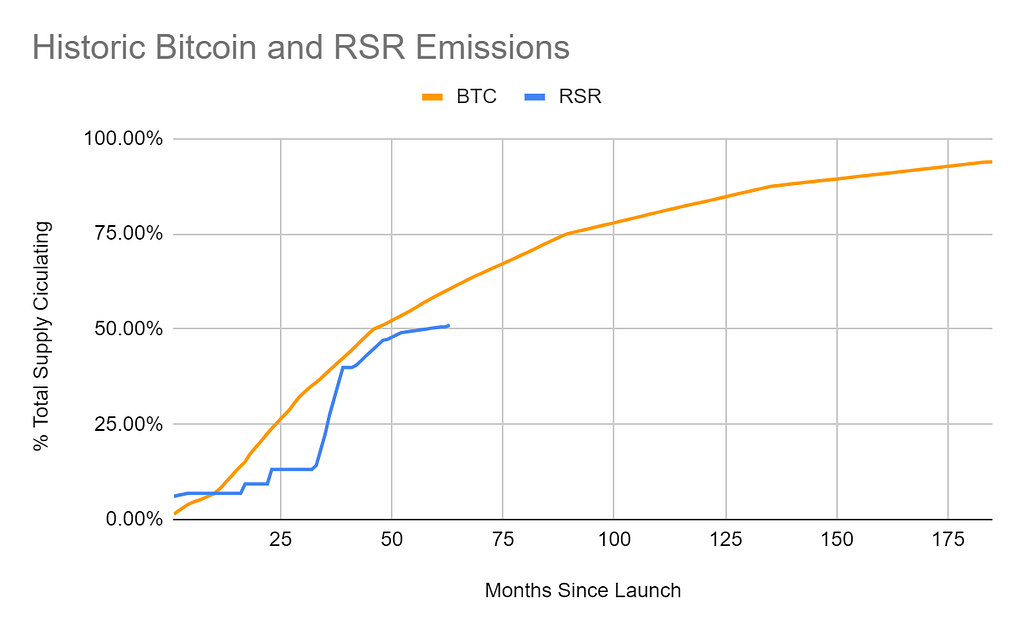

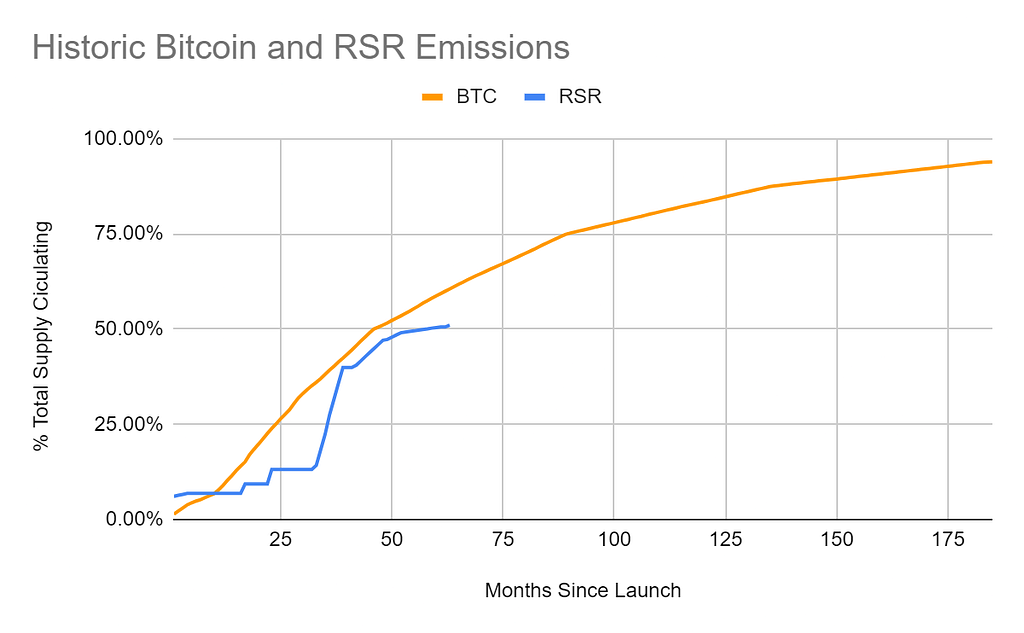

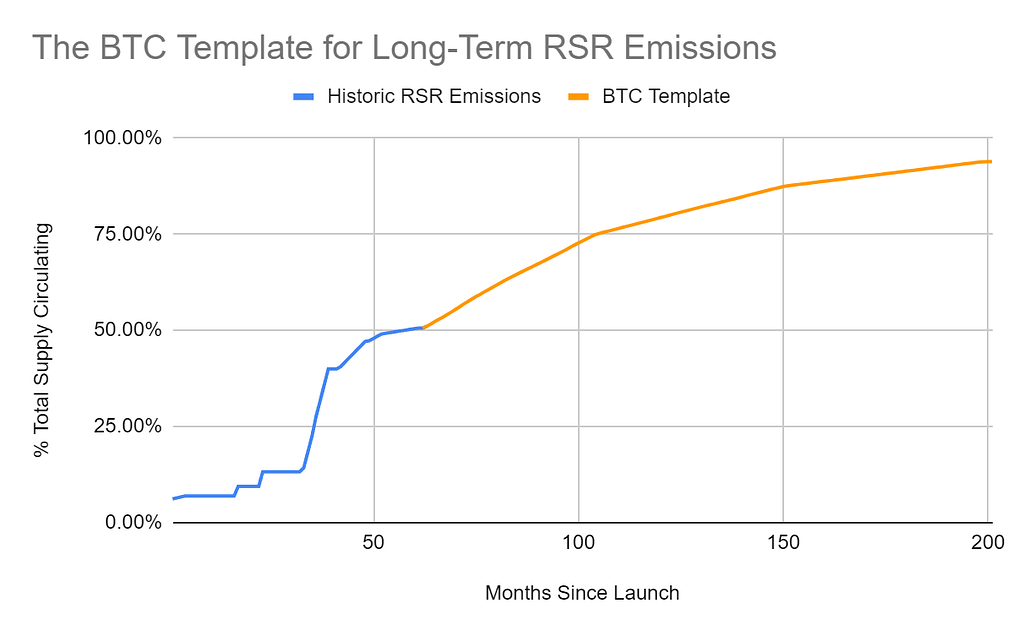

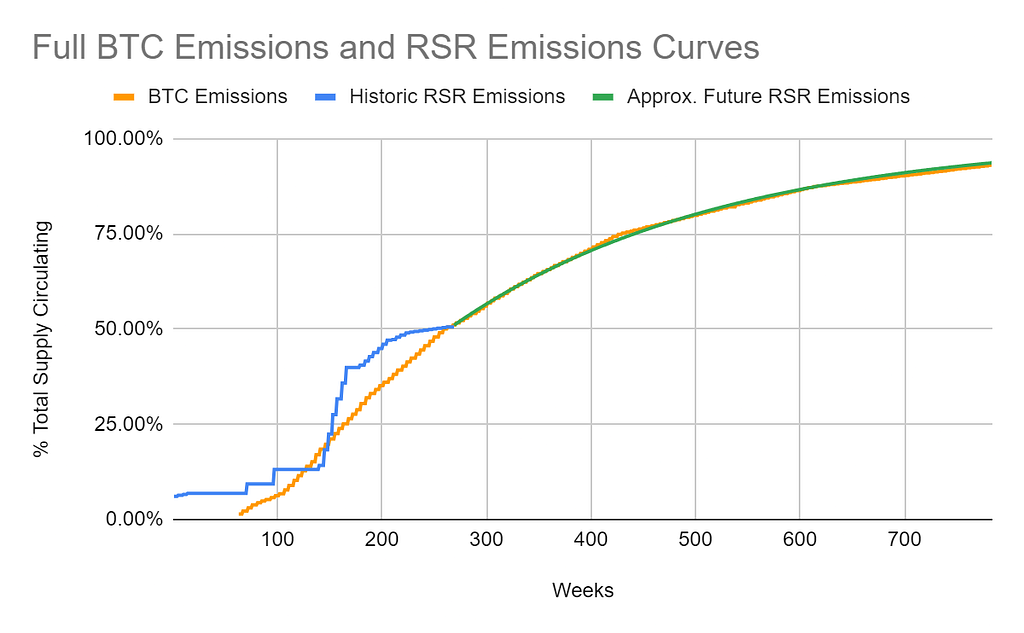

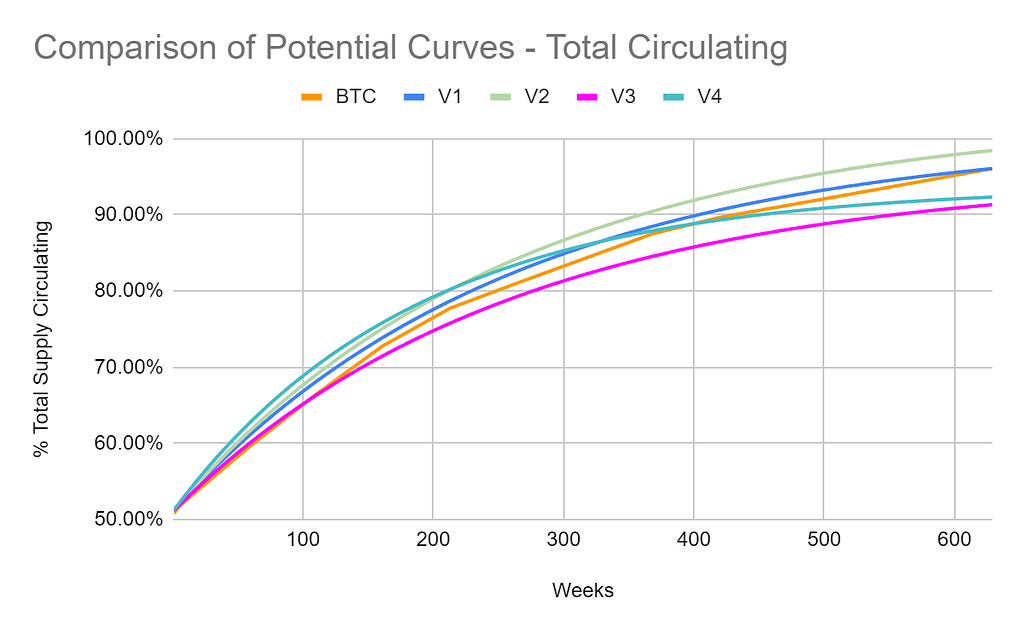

Here’s a comparison of the historical BTC and RSR emission curves:

Moving forward, the RSR emission curve will look approximately like the following — emulating the slope of BTC’s emissions from the 50% point on:

Note that Bitcoin emissions last until roughly 2140, though we’re already at around 94% of total BTC emitted today. We’re omitting the long tail in all of these charts so it’s easier to see the action in the earlier period, but the full RSR emissions curve will last a long time as well.

Note that Bitcoin emissions last until roughly 2140, though we’re already at around 94% of total BTC emitted today. We’re omitting the long tail in all of these charts so it’s easier to see the action in the earlier period, but the full RSR emissions curve will last a long time as well.

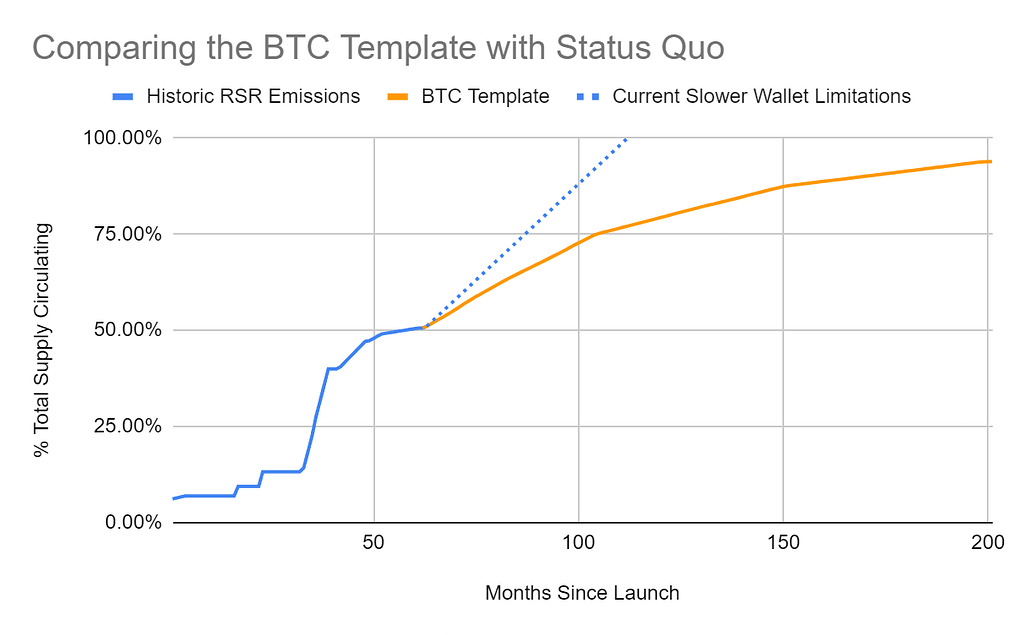

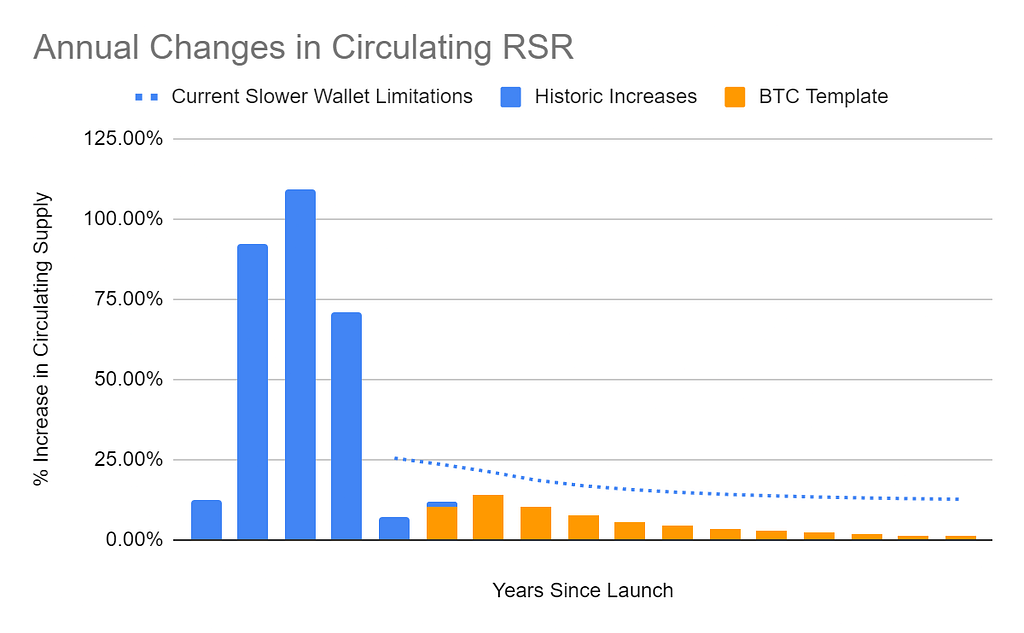

This represents a reduction in the RSR that can be emitted per unit time, as this approach will replace the more flexible “Slower Wallet” system (which allows Confusion Capital to withdraw up to 1% of total RSR every four weeks) with a lower, deterministic curve.

Here’s a visual comparison:

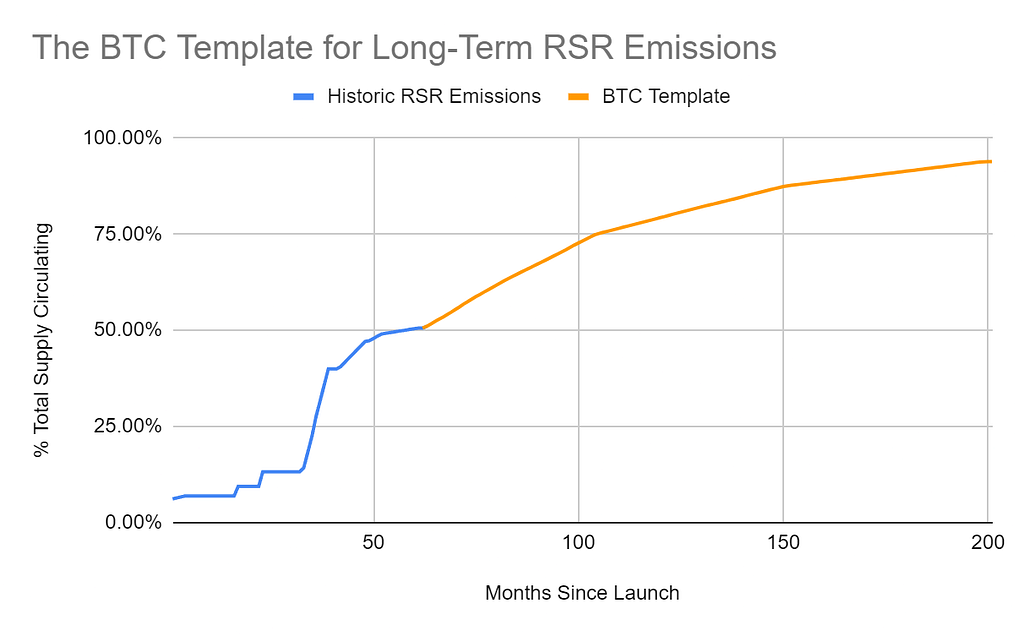

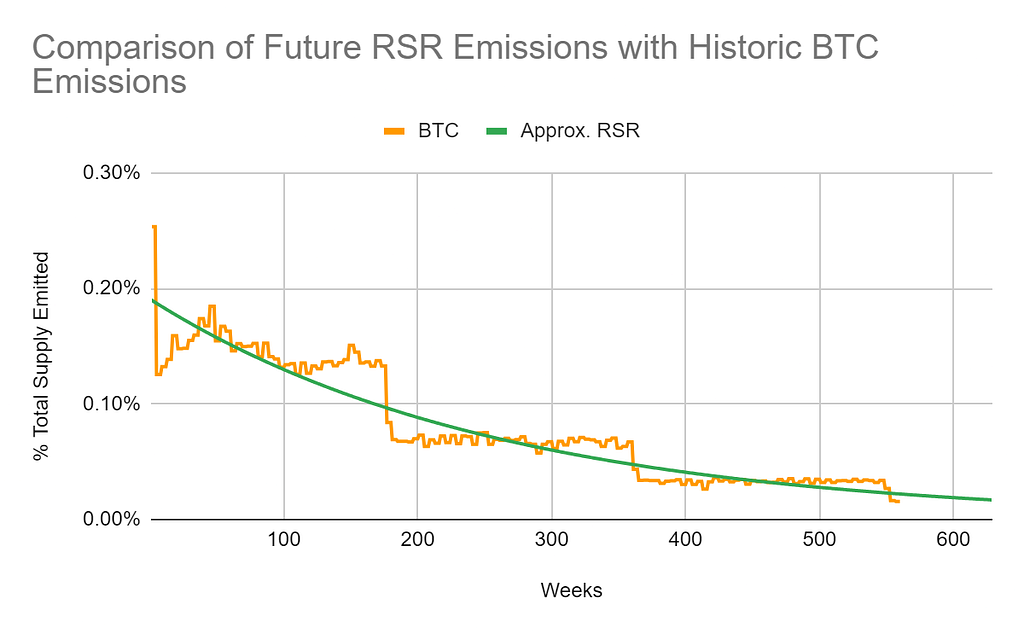

It also represents a clear reduction relative to past emissions. Here’s a comparison of historic RSR emissions to what future RSR emissions will look like with this approach:

As you can see, future increases in circulating supply will come nowhere close to the rate of past increases.

This plan was discussed at Monetarium and received broad support. Thanks to everyone who participated!

As a refresher for those not following closely:

- About 50% of RSR has been distributed so far to bootstrap the Reserve project

- About 50% remains to be distributed

- There’s a lot more work to be done if the Reserve ecosystem is to achieve its long-term ambition: producing an asset-backed world reserve currency

- Only 100 billion RSR exist and no more RSR can ever be created — RSR is a fixed-supply asset, with no ability for anyone to upgrade or change its implementation smart contract

The body of this post goes into quite a lot of detail on the reasoning behind the plan and how it will be implemented, but first let’s look at what currently happens to RSR when it’s emitted.

How emitted RSR is used

You might wonder: is a big chunk of the RSR that’s emitted just insta-dumped?

No, none of the RSR that’s emitted is insta-dumped.

Each emissions period (weekly — more detail on intervals later in the post), this is what currently happens:

- Confusion Capital unlocks a chunk of tokens

- Most of this RSR is divvied up and sent to ABC Labs and Best Friend Finance

- These companies receive the tokens and pay them out directly in RSR, without selling any

- Some of this RSR is spent on compensating full-time project contributors for their work and incentivizing DeFi market participants for holding and providing liquidity on RTokens

- Some RSR is held by ABC Labs and staked on RTokens to generate revenue

- Confusion Capital holds onto the RSR that isn’t distributed to ABC Labs and Best Friend Finance

- In the course of a typical withdrawal, Confusion Capital doesn’t sell any RSR for cash

This is how things currently work. At the bottom of this post you’ll find a discussion about how allocation of RSR emissions can and should evolve.

How much eventually gets sold?

Periodically, Confusion Capital will consider whether it makes sense to buy or sell some RSR. Generally speaking, it will only consider placing RSR sales once every few years when markets are up and making RSR purchases once every few years when markets are down.

Our long-term aim is for Confusion Capital, ABC Labs, and Best Friend Finance operations to be fully funded by other means, with no need to sell any further RSR. That said, depending on how each piece of the project is going and on the conditions of the market, there may be times where it makes sense for Confusion Capital to top up its cash reserves through selling RSR, or top up its RSR reserves by making purchases on the open market.

We don’t currently need to sell any RSR in an ongoing way because in the past we sold at favorable prices during strong market conditions (passively over the course of several months). Hence we have not needed to sell any RSR to fund operations for quite a long time, and at the moment have no short-term need to sell any RSR.

When project contributors and DeFi market participants receive RSR, it’s unlocked and they are free to do what they wish with it. Some full-time contributors receiving RSR need to sell some as they receive it in order to cover income taxes, so that’s one regular source of some secondary RSR selling in response to emissions. A good bit of the RSR that’s distributed to external market participants as an incentive for holding and providing liquidity on RTokens gets sold (according to our onchain observations), and in response we’ve been switching to paying these incentives out of our cash reserves instead, with payments made in RTokens.

Historically, the vast majority of RSR that’s been sold on open markets has been transacted slowly over long periods of time, during periods of market strength. We have never and would never market-sell a big chunk of RSR, since it’s of course in the project’s interest for RSR to retain its market strength as the backstop collateral asset for the Reserve ecosystem.

Our overall position

I personally believe Reserve is in an excellent RSR supply position given the stage of the project.

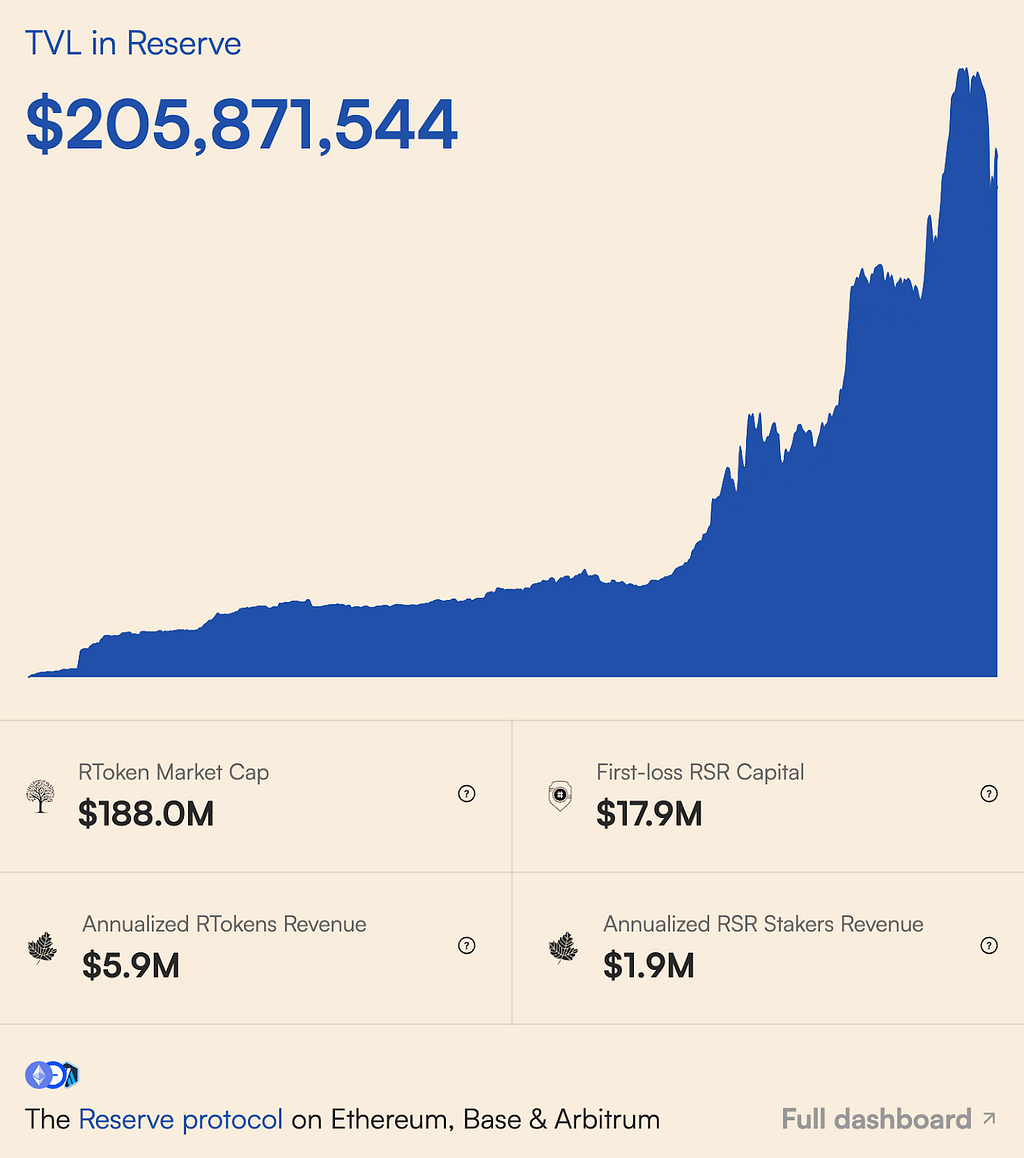

We’ve distributed half of the token supply in order to invest years of rigorous system design, complete 9+ audits, and bootstrap initial traction, along with funding the creation of RPay and now Ugly Cash. The protocol is in use and the smart contracts are demonstrating their ability to safely hold an increasing value of funds — about $200 million as of recent weeks.

Reserve TVL as of August 9th, 2024

Reserve TVL as of August 9th, 2024

I’m really excited and pleased to be in this position, and I think this emissions plan sets the ecosystem on a great course for the long-term future of the project.

BTC’s predictable release and fixed supply have been essential to its acceptance as a reliable store of value. This stability influences the market directly and resonates strongly with the community. For Reserve to fulfill its vision, RSR needs to embody the same level of stability and trustworthiness as Bitcoin.

For those who want more details and rationale, please read below and ask any questions you might have on the corresponding forum thread. Thank you again to everyone who contributed online and in person to thinking this through!

The rest of this post will cover:

- Lessons from crypto history so far

- Key conclusions we reached during this discussion

- The RSR emissions curve

- How this all will be implemented

- How emitted RSR will be allocated

Lessons from crypto history so far

RSR is not operating in a vacuum; there are new experiments being tested each day as the crypto industry grinds for product-market fit and sustainable governance. Here are some of the most important lessons from the past seven years of crypto experiments (and the past 15 years of Bitcoin) that RSR holders had in mind when discussing how to approach emissions:

1. Token supply must grow more slowly than demand

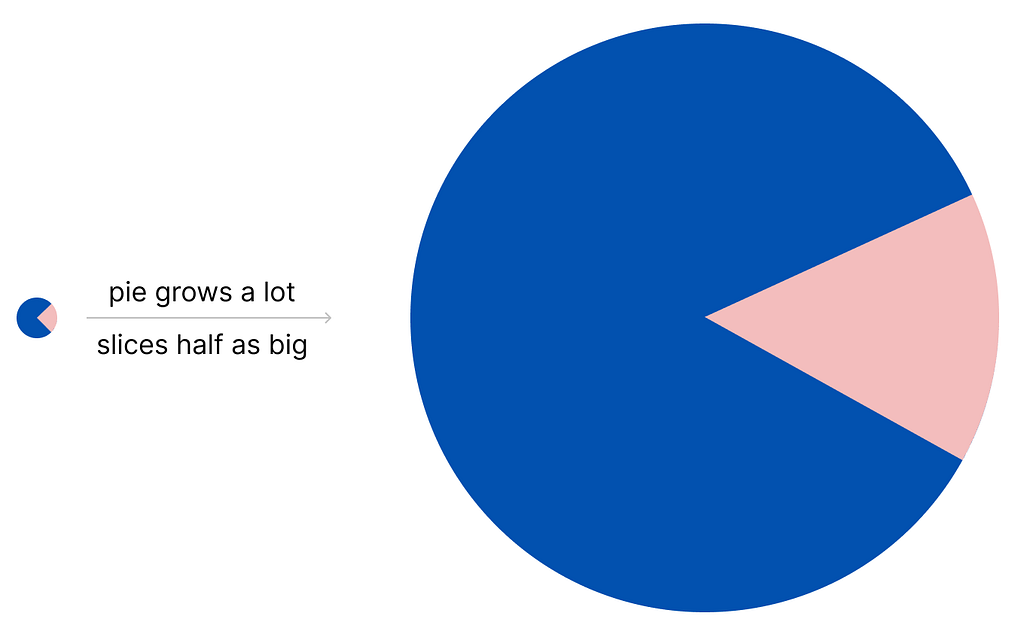

As covered in our earlier blog post, many cryptoassets that have been released over the past seven years have underperformed BTC in token price, even though their market caps have outperformed BTC’s market cap growth.

Put simply: while these other cryptoassets’ overall “pies” grew faster than BTC, each holder’s “slice of the pie” shrunk more quickly than the pie grew.

As you can see in the diagram above:

- Without the shrinking slice size, the other cryptoassets would have been a better bet than BTC

- With the shrinkage, they were a worse bet

More tokens coming out is what diluted current holders and shrunk everyone’s slice of pie.

Programming supply to reliably grow more slowly than demand would require knowing how quickly demand will grow. In crypto, demand is volatile and can be hard to predict.

But somehow (with no comparative examples to go off of!) Satoshi got it right, programming an emissions schedule that was aggressive enough to incentivize sufficient mining even early on, but gentle enough not to overwhelm growth in demand once BTC started to attract holders.

The stable, deterministic, and declining emissions curve of Bitcoin enabled demand for BTC to outpace its supply.

2. The meme matters as much as the reality

Assets that have attractive supply dynamics benefit from both (a) the actual mechanistic market impacts as well as (b) people falling in love with the guarantee offered by the supply dynamic and talking about it with others.

Before crypto we had gold, the OG limited-supply asset. Gold bugs have been going on for decades about how we should go back to the gold standard, and investors have long been holding gold as a hedge against USD inflation.

Check out the recent talk on the Gold Standard @ Monetarium 1— it’s pretty convincing!

Then we have Bitcoin’s 21 million coins. How many times have you been reminded of its capped supply? I’ve heard it hundreds of times now. The meme was so powerful it made a meaningless digital balance with no intrinsic value into a trillion-dollar asset.

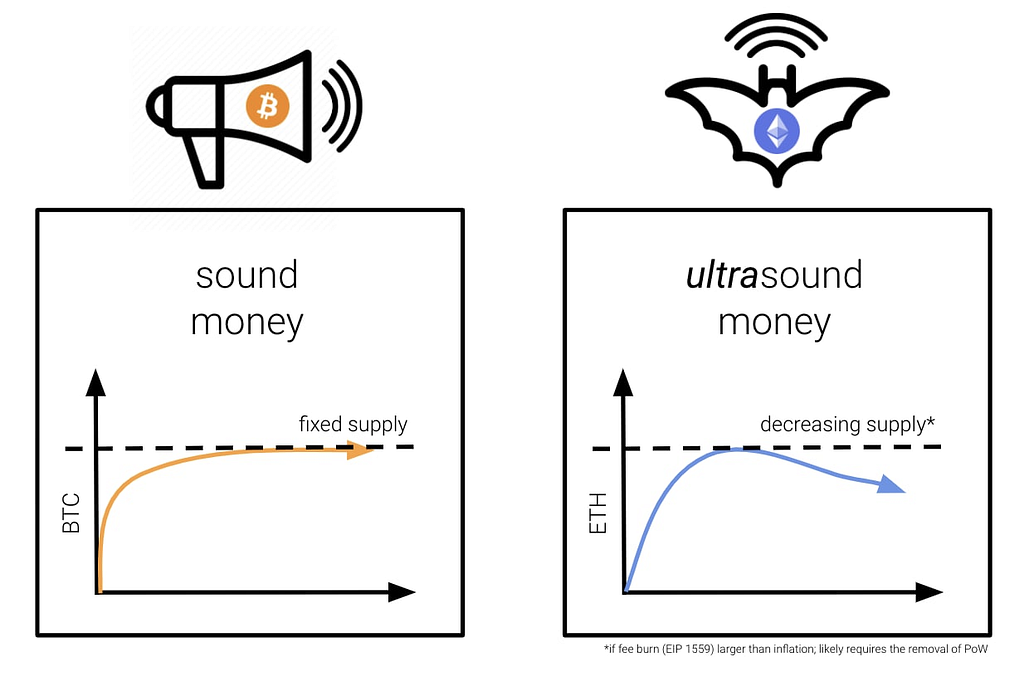

The Ethereum community eventually followed. Do you recognize 🦇🔊?

You can’t go anywhere on CT without running into this meme right in usernames. Their idea with “ultrasound money” is to drive supply down over time:

In all these cases, it’s not just that certain supply dynamics have a mechanistic market impact, it’s also that they’re simple enough to understand and remember, and they’re touted over and over and over again. They’re memetic.

3. Incentives can supercharge growth in DeFi, but come with downsides

Incentivizing early usage in DeFi has become a necessary strategy that every project must engage in. When done well, it clearly works. Pretty much any time you hear about a project reaching an exciting early pop in usage there are incentives involved. This is true of Reserve’s recent growth.

But yield farming arrangements that depend on a token’s price can be reflexive, winding down in bear markets as quickly as they go up in the bull.

Compound pioneered yield farming, and you can see when it started in mid-2020 when its TVL massively jumped:

This chart is ETH-denominated so you can see the TVL and COMP token price adjusted for crypto bull/bear cycles. Price and TVL both go down more than ETH price does.

Yield farming capital is mercenary and will leave as soon as something’s no longer the best opportunity, so a successful incentivized growth approach needs to capitalize on big numbers to create lasting value and infrastructure for the project’s ecosystem. If a DeFi app gets integrated into 20 other DeFi ecosystems while it’s on a fast and exciting growth trajectory, that positions it for more organic usage once incentives are reduced.

Many projects have paid for growth incentives by rapidly growing the circulating supply, outpacing demand growth even for an exciting project. This leads to the token declining in price, which reduces incentives, reducing TVL and reducing demand.

So we can’t overdo it. Rapid growth can quickly turn into rapid decline.

4. If a token isn’t going up, it’s going down

Many in crypto are looking for short-term gains, so if something isn’t going up, or it’s going up more slowly than something else, they’ll trade.

The result? If a token isn’t keeping up with the market for a while, that effect can compound into a vicious cycle as more people get anxious or bored and decide to sell.

On the flipside, if a token is outpacing the market for long enough, it’ll attract more buyers and continue to outpace the market until it’s exhausted the available buyer population.

These mini booms and busts are an unavoidable part of a token’s early life in crypto, so whether you like them or not, you have to plan for them and consider the impact that actions or systems will have on this phenomenon.

This relates to emissions because any period of fast emissions that outpaces demand and drives down price could have a compounding negative impact for months by driving cycles of further selling. On the other hand, a clean emissions schedule that has no FUD points and no instances of rapid unlocking can reduce the boom and bust dynamics by reducing need for short-term trading and building confidence over time.

5. While short-term buyers are driven by short-term narratives, long-term holders are driven by real mission and real value

Splashy incentives, big fundraises, and new big trends get headlines and bring in buyers. But many projects that have had their day in the sun end up quickly fading away.

For those that are focused on a big, bold mission like Reserve, keeping the mission in mind and creating real value for the long term is the only way to survive and grow.

Why? Because long-term survival and growth require committed long-term holders. Long-term holders track long-term narratives.

So while a long-term project must care about short-term narratives, it must also always keep track of long-term narratives, which are always ultimately driven by fundamentals.

One key long-term fundamental is how a token is emitted. By locking in a smooth long-term emissions curve, our ecosystem is providing confidence to long-term holders that they will never be suddenly diluted — the same confidence that BTC holders enjoy.

Key conclusions we’ve reached

Our initial blog post started this discussion by describing a very broad spectrum of possibilities so we could have a wide-ranging discussion about what would be best, then narrow things down from there once we’d heard from many people with different viewpoints. I’ve found many of the viewpoints interesting and stimulating — thanks to everyone who’s shared a take!

Upon considering the wide range of suggestions, we reached the plan we’re sharing today by coming up with clear arguments for four things not to do:

- Don’t burn the remaining RSR

- Don’t emit the RSR too quickly

- Don’t emit the RSR too slowly

- Don’t emit the RSR in volatile chunks

1. Don’t burn the remaining RSR

While burning the remaining half of supply would 2X each RSR’s future share of RToken staking rewards, we believe not allocating that half to ecosystem growth and development might prevent RTokens from reaching even a fraction of their potential market cap. In this future, slices of the pie would stay the same size (since circulating supply could no longer grow), while RToken market cap and staking opportunities might not grow much:

By contrast, if the second half of the supply were well-utilized by the Reserve ecosystem, each RSR holder’s share of the circulating RSR would go down by ≈50% as further RSR is emitted, but the total RToken market cap and staking opportunities may significantly surpass 2X:

Obviously we do not know what will happen to the overall “pie” of RTokens to stake on in the future and I make no promises one way or the other, but here’s our thinking on why this capital allocation opportunity is so important:

There’s still a ton of work the Reserve ecosystem has in front of it if we’re going to achieve our long term goal of asset-backed currency, including:

- Core development

- Front end development

- Protocol research and evolution

- RToken governance research and design

- Reserve ecosystem design

- Audits

- Marketing and education

- Platform integrations

- DeFi integrations

- Legal analysis

- Financial policy development and advocacy

- Planning and executing integration into the traditional economy

- Legitimacy building

- Crisis response

- Miscellaneous additional functions that support the work above (graphic design, accounting, compliance, recruiting, and many many more)

- Other challenges we haven’t thought of yet

We noticed that those in favor of burning part or all of the remaining RSR may be discounting or ignoring all the work that still needs to happen, so I went through these categories in more detail in the presentation at Monetarium. Check out the section where I list everything:

Who will do all this work?

Well, we don’t know, but:

- People don’t tend to do hard work for free

- Taxing RTokens in order to pay for the work that will go into maintaining and improving the whole ecosystem is a lot more difficult than just very slowly emitting RSR

Think about it: how many of Ethereum’s improvements are developed for free? How many of them are paid for with Ethereum transaction fees? The answer to both is: pretty much none. My understanding is that they’ve been paid for largely by the foundation making grants of ETH (or cash from having sold some of its ETH). If the foundation had just burned all this ETH earlier on, that would clearly have been a net loss to the ecosystem.

Historically, the first 50% of RSR was spent roughly as follows:

- 20% to core team and advisors to reach protocol launch

- 13.4% to initial investors to pay for 2018–2019 activities

- 17.1% spent since for 2019–2024 activities

- Total: ≈50% of RSR emitted

From this spending, the Reserve ecosystem:

- Launched RPay, growing to hundreds of thousands of people using stablecoins for everyday purchases, amounting to billions transacted (though were ultimately forced to pivot)

- Launched the Reserve protocol

- Grew RTokens to their current size

- Built Ugly Cash, which is about to fully launch

With ≈50% of the RSR left to allocate, but with each RSR being a lot more valuable than they were at the start, we are positioned well to take a crack at our ambitious goal.

2. Don’t emit the RSR too quickly

This one’s pretty obvious. Growing supply faster than demand reduces the value of each token, so nobody wants that. See lesson #1 above: Token supply must grow more slowly than demand.

3. Don’t emit the RSR too slowly

One clear reason not to emit too slowly is that we must somehow fund all of the progress needed in order to achieve our goal. Building and growing too slowly would be bad for project momentum, and things could unwind. So we must keep things moving at a good pace.

But there’s also a more subtle issue with emitting too slowly: growing supply too slowly relative to demand growth can lead to unreasonable prices for each token for a period of time. This results in some people buying the token at a price that it may take a long time to reach again (as in, buying an irrationally high top), so unless they are a super-committed long-term holder, they’ll end up selling at a loss and moving on. This is not healthy for the ecosystem.

4. Don’t emit the RSR in volatile chunks

Emitting big chunks at a time is essentially a combo of the two problems above — you can have a good long-term trendline, but if emissions happen too slowly for a while and then too quickly for a while, you get prices going high and then dilution happening too fast. So we must worry not only about the average over time, but the smoothness of the schedule.

Again, for a little more color on these ideas, check out the presentation from Monetarium.

The RSR Emissions Curve

With the above lessons and principles in mind, we’ve decided to adopt a long-term RSR emissions curve which emulates Bitcoin emissions beginning at the corresponding point in Bitcoin’s history.

Bitcoin reached 50% circulation in November 2012. RSR reached 50% circulation in February 2024. At this point in RSR’s history, the supply has actually grown more slowly than Bitcoin on average.

However, while Bitcoin was emitted on a relatively smooth curve, RSR supply grew in volatile chunks. As the chart above shows, some months RSR had no emissions, while other months it was released quickly. This is not something we want to repeat.

By adopting a long-term emissions curve which emulates Bitcoin, RSR emissions will look roughly like the following:

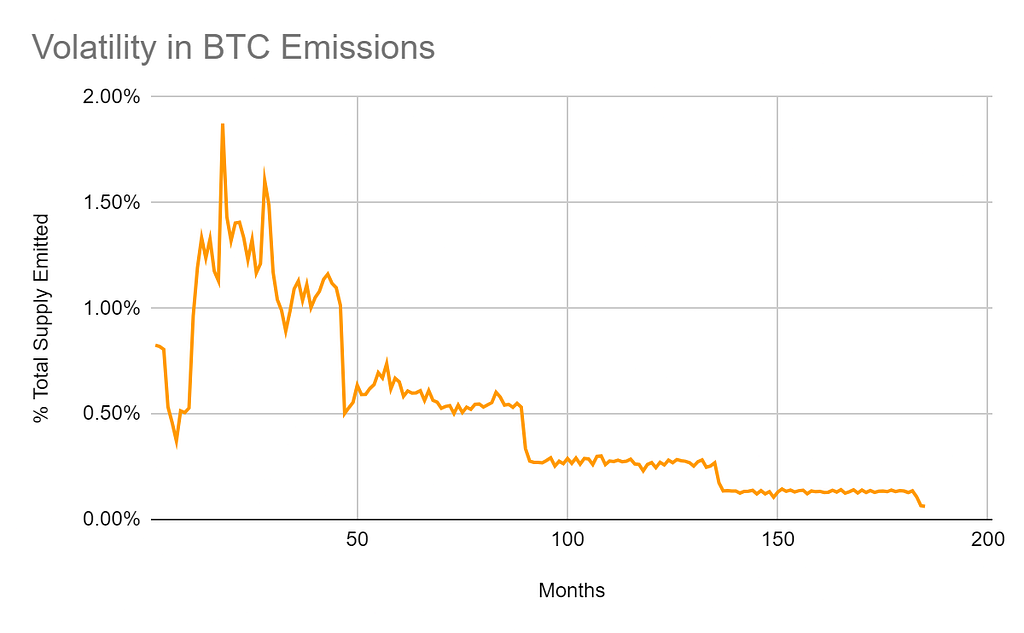

While Bitcoin’s emission rate appears smooth over the long term, it is actually quite volatile month to month. Within certain periods, emissions swing by as much as 30% from one month to the next:

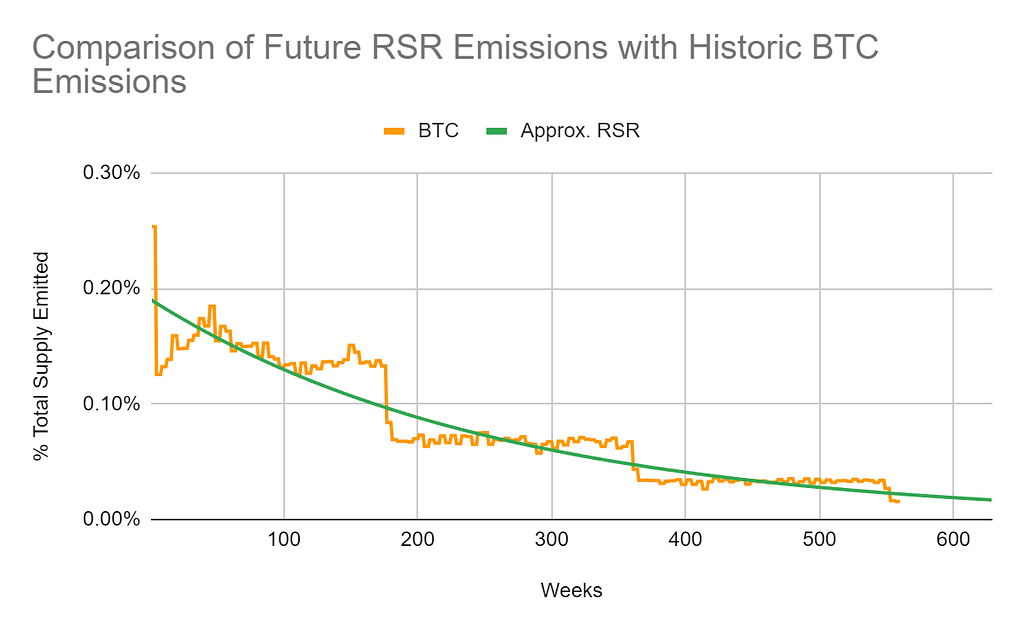

For this reason, we have elected to emulate Bitcoin’s supply without replicating the volatility. This chart begins when Bitcoin and RSR are both ≈50% emitted.

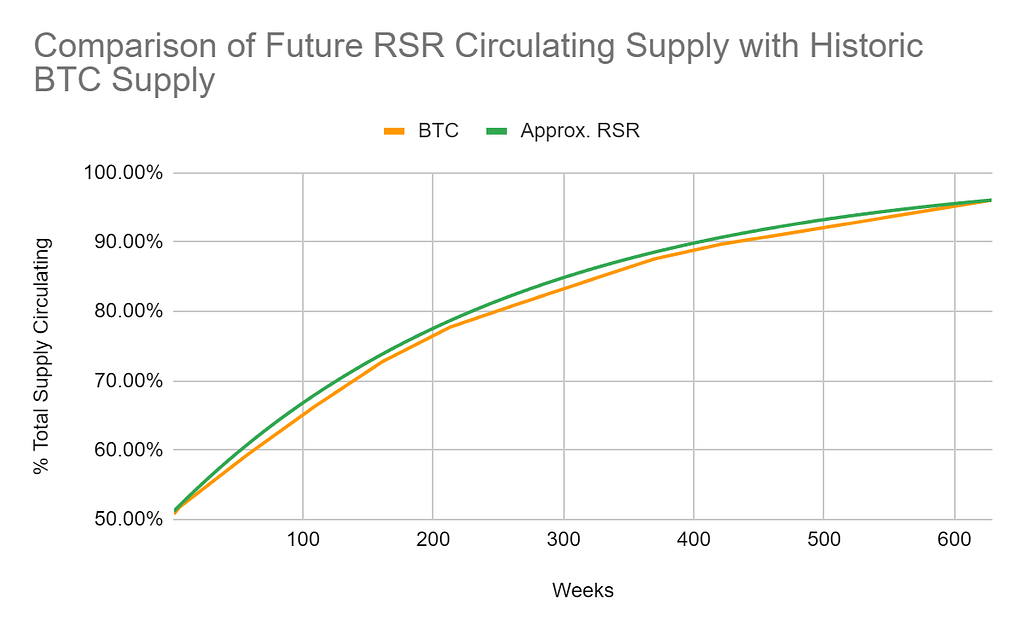

The cumulative curve with this smooth approach follows Bitcoin pretty closely:

Thus, the RSR curve will look approximately like the following:

How this will be implemented

Starting in four weeks, Confusion Capital will begin making weekly withdrawals of RSR from the Slower Wallet.

While these emissions will be manual to start, they will be hardcoded in coming months, so that all remaining RSR will be cryptographically secured for deterministic release, with nobody (not even Confusion Capital) having any power to release them any more quickly.

We don’t have an exact timeframe for developing the emissions smart contract, as any smart contract development must be done slowly and carefully and must receive audits, but we aim to get this finished as soon as possible, since providing full certainty to every RSR holder is very valuable for the project.

In our discussions at Monetarium, many of you asked that the curve be as near continuous as possible. For this reason, during the manual withdrawal phase we will be conducting withdrawals on a weekly pace, aiming to decrease FUD points and smooth new tokens entering circulation. While daily or block-by-block would be even smoother, the gas and operational overhead would be too high.

Before hardcoding this curve forever, a few additional details we need to finalize include:

- Determining the release frequency (e.g. weekly, daily, continuous, etc. — the hardcoded version could have a different cadence than the manual withdrawals we will begin with)

- Finalizing how long the hardcoded curve will last — should it have a longer tail than BTC, emitting a tiny amount for 1000 years?

- Determining whether the hardcoded curve should have any dislocations (e.g. like Bitcoin’s halvings) or not

- Working out technical details of how exactly the contract will work

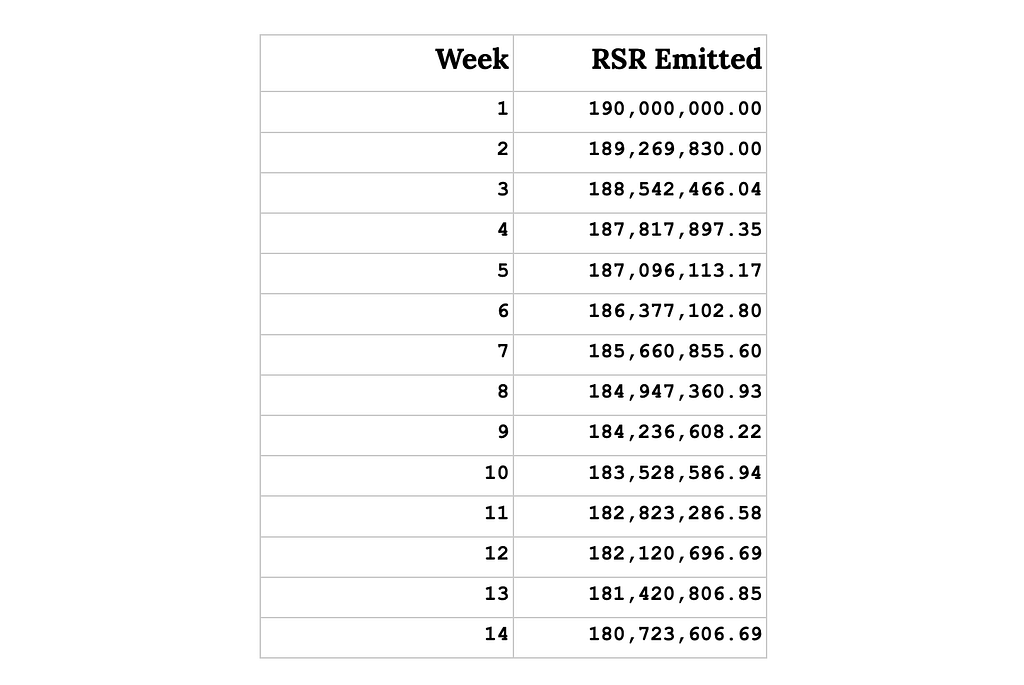

While small details may shift between now and hard-coded implementation, all manual emissions will follow this exact procedure and formula:

- Withdrawal period: weekly

- Initial weekly withdrawal amount: 0.19% of the total supply, or 190,000,000.00 RSR

- Weekly withdrawal depreciation: each weekly withdrawal will be 99.6157% of the previous week

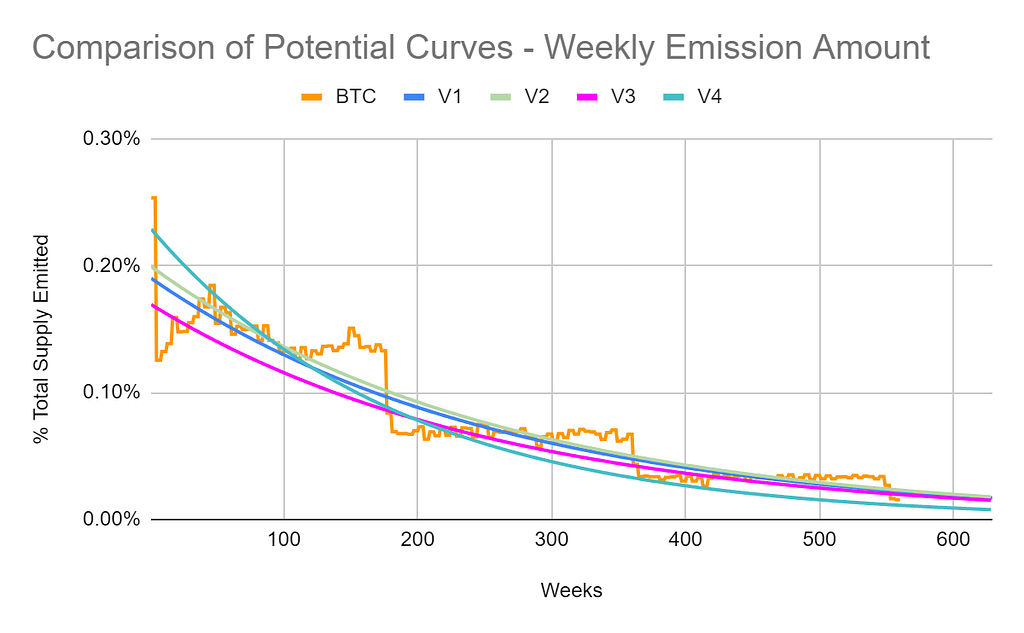

Here is the shape of the resulting smooth curve in relation to BTC emissions:

Using this formula, for the next three months (beginning four weeks from now — recall that the Slower Wallet has a 4-week delay in withdrawals), weekly RSR emissions will be:

While there may be some slight variability in the manual and hardcoded curves as details are finalized, the final curve will still closely emulate Bitcoin’s overall supply dynamic. Here are some comparisons of possible final curves, for reference:

Transferring RSR from the Slow and Slower Wallets

Once the final emissions contract is ready, we’ll take two actions to place all remaining RSR under its control:

- Transfer in all of the RSR from the Slow Wallet

- Irrevocably link up the Slower Wallet to the emissions contract

That second step is a little more complicated than a simple transfer. Because the Slower Wallet has no way of releasing RSR any faster than its upper-bounded limit, it’s not possible to quickly transfer all its RSR into the emissions contract up front. But there’s still a way to provide full hardcoded certainty, because we anticipated wanting to give away control like this. Here’s how that works:

- The Slower Wallet can be set by its admin to only be able to process withdrawals to a single address

- The Slower Wallet can be set by its admin to allow anyone to create withdrawal transactions to that single, defined address

- The admin role can relinquish its power, irrevocably

- This allows the admin to connect the Slower Wallet to an emissions contract (as the sole possible recipient), allow anyone to initiate those transfers to the emissions contract, and then relinquish its admin powers

- This irrevocably funnels all Slower Wallet RSR through the emissions contract, thus subordinating the emissions rate to the emissions contract’s logic forever

How emitted RSR will be allocated

A separate question from how quickly RSR will be emitted is how it will be allocated.

As noted in the introduction to this post, each emissions period, this is what happens:

- Confusion Capital unlocks a chunk of tokens

- Most of these tokens are divvied up and sent to ABC Labs and Best Friend Finance

- These companies receive the tokens and pay them out directly in RSR, without selling any

- Some of these RSR are spent on compensating full-time project contributors for their work and incentivizing DeFi market participants for holding and providing liquidity on RTokens

- Some RSR are held by ABC Labs and staked on RTokens in order to generate revenue

- Confusion Capital holds onto the RSR that aren’t distributed to ABC Labs and Best Friend Finance

- In the course of a typical withdrawal, Confusion Capital doesn’t sell any RSR for cash

This is how it works today, but this will change over time.

In January we raised an idea for discussion:

Idea: 20b RSR for incentives? ABC Labs and Confusion Capital are exploring how to make the best use of the remaining supply of RSR, and are seeking your input on a potential direction that’s under consideration: allocating 20 billion RSR to an emissions contract that would release it smoothly over many years, directed by RSR holders to whichever incentive programs and bootstrapping costs they choose over time, similar to CRV emissions voted on by veCRV holders and directed to incentivize Curve LPs.

The analysis of this idea continues, in the community and within ABC Labs. The ABC team has already started writing code to enable this plan, but they’re also still investigating pros and cons of different ways RSR can be used to grow and establish the Reserve monetary system, so that code may not see the light of day. It’s a huge commitment to make one way or the other. Input from all RSR holders is of course still welcome.

(To be clear, any RSR allocated this way would be subject to the exact same emissions curve. It would come out of an emissions contract and only then be allocated by RSR holders.)

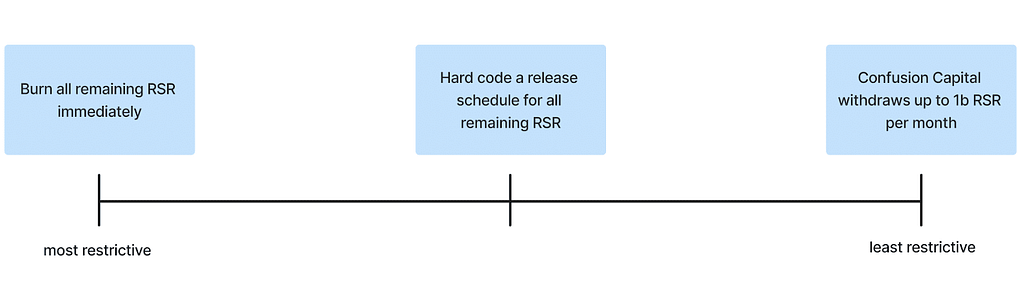

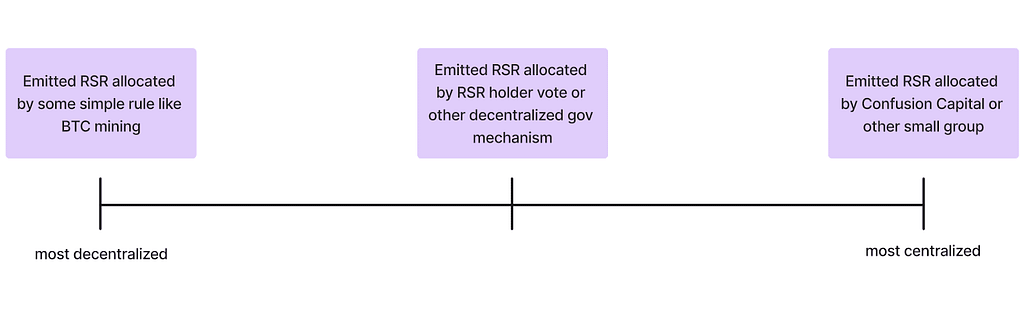

When we struck up the conversation about emissions on the forum, we highlighted two spectra we needed to make a decision on.

The rate of emissions:

And how emissions are allocated:

With today’s announcement we’re establishing a clear plan for the rate of emissions (right in the middle of the spectrum!), but we’re still leaving the door open for discussion on how emissions should be allocated in the future.

On one end of the spectrum is the most centralized path: simply have Confusion Capital or some other small group allocate the RSR. In contrast, we have the most decentralized, in which emitted RSR is allocated by some simple rule which can’t be changed, like flowing to all RToken holders and/or RSR stakers pro-rata. Somewhere in the middle of these two poles is the creation of some other decentralized, flexible method to allocate RSR.

It’s a hard question, and the mechanism(s) may need to evolve over time.

We’ve just posted a new forum thread today to ignite further discussion on the allocation question:

Discussion: RSR Allocation Mechanisms for the Future

Looking ahead

Despite some challenges we’ve endured in reaching this point, we are in a really great position in my opinion.

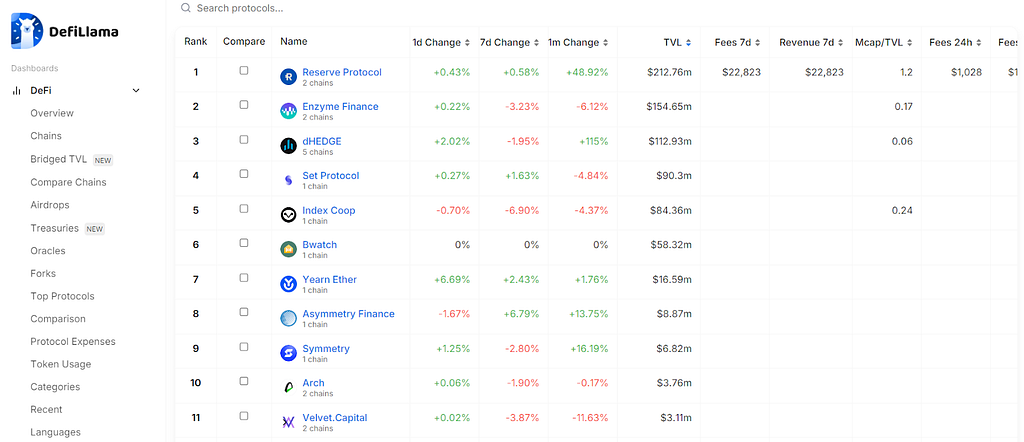

The protocol has ≈$200M in TVL, making it the #1 index platform in DeFi across all chains:

Meanwhile, Ugly Cash is getting close to its full launch, RSR’s market cap is in the neighborhood of BTC’s when it reached 50% circulating, and we still have ≈50% of the RSR supply to allocate in order to reach our end-goal of enabling asset-backed currency.

LFB.

Nevin Freeman President, Confusion Capital

Action steps for those who want to engage:

- Ask any questions you have about the emissions plan here: Discussion: Q&A for the new RSR Emissions Curve

- Discuss the best ways to allocate RSR moving forward here: Discussion: RSR Allocation Mechanisms for the Future

SHARE THIS